etf <- etf_vix[1:55, 1:3]

# Split-------------------------------

h <- 5

etf_eval <- divide_ts(etf, h)

etf_train <- etf_eval$train

etf_test <- etf_eval$testModels with Stochastic Volatilities

By specifying cov_spec = set_sv(),

var_bayes() and vhar_bayes() fits VAR-SV and

VHAR-SV with shrinkage priors, respectively.

- Three different prior for innovation covariance, and specify through

coef_spec- Minneosta prior

- BVAR:

set_bvar() - BVHAR:

set_bvhar()andset_weight_bvhar()

- BVAR:

- SSVS prior:

set_ssvs() - Horseshoe prior:

set_horseshoe() - NG prior:

set_ng() - DL prior:

set_dl()

- Minneosta prior

-

sv_spec: prior settings for SV,set_sv() -

intercept: prior for constant term,set_intercept()

set_sv()

#> Model Specification for SV with Cholesky Prior

#>

#> Parameters: Contemporaneous coefficients, State variance, Initial state

#> Prior: Cholesky

#> ========================================================

#> Setting for 'shape':

#> [1] rep(3, dim)

#>

#> Setting for 'scale':

#> [1] rep(0.01, dim)

#>

#> Setting for 'initial_mean':

#> [1] rep(1, dim)

#>

#> Setting for 'initial_prec':

#> [1] 0.1 * diag(dim)SSVS

(fit_ssvs <- vhar_bayes(etf_train, num_chains = 2, num_iter = 20, coef_spec = set_ssvs(), cov_spec = set_sv(), include_mean = FALSE, minnesota = "longrun"))

#> Call:

#> vhar_bayes(y = etf_train, num_chains = 2, num_iter = 20, coef_spec = set_ssvs(),

#> cov_spec = set_sv(), include_mean = FALSE, minnesota = "longrun")

#>

#> BVHAR with Stochastic Volatility

#> Fitted by Gibbs sampling

#> Number of chains: 2

#> Total number of iteration: 20

#> Number of burn-in: 10

#> ====================================================

#>

#> Parameter Record:

#> # A draws_df: 10 iterations, 2 chains, and 210 variables

#> phi[1] phi[2] phi[3] phi[4] phi[5] phi[6] phi[7] phi[8]

#> 1 0.8983 -0.0599 0.0916 -1.865 -0.08285 -0.65925 -0.223 1.60857

#> 2 0.1141 0.4634 -0.0177 -0.455 -0.02866 -0.70327 0.301 1.19827

#> 3 0.4094 0.1782 -0.0727 0.293 -0.08276 0.14471 -2.338 -0.01015

#> 4 -0.7451 -0.1365 -0.0405 0.230 0.30052 -0.39210 -0.431 -0.00581

#> 5 -0.3590 0.1685 -0.0122 0.556 0.13990 -0.09000 -0.308 0.14631

#> 6 0.4698 -0.3892 0.0172 -0.449 0.10019 -0.23203 0.387 0.08415

#> 7 -0.0563 -0.0740 0.0171 0.375 0.20512 0.00926 0.053 0.32945

#> 8 0.0203 0.0580 -0.0556 0.453 0.36827 -0.09601 0.103 0.04103

#> 9 -0.0478 0.0260 -0.0415 0.386 -0.01221 -0.17503 0.219 -0.00532

#> 10 0.0488 0.0445 -0.0428 0.024 0.00395 -0.06741 0.288 0.20163

#> # ... with 10 more draws, and 202 more variables

#> # ... hidden reserved variables {'.chain', '.iteration', '.draw'}Horseshoe

(fit_hs <- vhar_bayes(etf_train, num_chains = 2, num_iter = 20, coef_spec = set_horseshoe(), cov_spec = set_sv(), include_mean = FALSE, minnesota = "longrun"))

#> Call:

#> vhar_bayes(y = etf_train, num_chains = 2, num_iter = 20, coef_spec = set_horseshoe(),

#> cov_spec = set_sv(), include_mean = FALSE, minnesota = "longrun")

#>

#> BVHAR with Stochastic Volatility

#> Fitted by Gibbs sampling

#> Number of chains: 2

#> Total number of iteration: 20

#> Number of burn-in: 10

#> ====================================================

#>

#> Parameter Record:

#> # A draws_df: 10 iterations, 2 chains, and 215 variables

#> phi[1] phi[2] phi[3] phi[4] phi[5] phi[6] phi[7] phi[8]

#> 1 0.2362 0.1463 -0.0517 -0.0742 -1.66e-03 -0.06187 0.1833 0.1611

#> 2 0.1831 0.1819 -0.1090 0.1610 8.89e-03 -0.00887 0.0232 0.1321

#> 3 0.2455 0.1286 -0.0703 0.1222 -8.73e-03 -0.05949 -0.1382 0.1039

#> 4 0.0963 0.1087 -0.1558 0.1166 5.65e-03 0.02191 0.1070 0.1130

#> 5 0.0372 0.1497 -0.1538 0.1946 -2.67e-03 -0.02359 -0.0237 0.2995

#> 6 -0.0573 0.1079 -0.2566 0.5879 7.73e-04 0.01944 0.0156 0.0960

#> 7 0.1053 0.0943 -0.1837 0.2004 1.80e-03 0.10304 0.0697 0.2996

#> 8 0.0232 -0.0412 -0.1501 0.3045 -2.18e-04 -0.13582 0.0191 -0.0158

#> 9 0.0504 0.1025 -0.1617 0.2406 9.16e-05 0.00157 -0.0346 0.2380

#> 10 0.0223 0.0831 -0.1558 0.1374 -1.42e-04 -0.01194 0.0992 0.1018

#> # ... with 10 more draws, and 207 more variables

#> # ... hidden reserved variables {'.chain', '.iteration', '.draw'}Normal-Gamma prior

(fit_ng <- vhar_bayes(etf_train, num_chains = 2, num_iter = 20, coef_spec = set_ng(), cov_spec = set_sv(), include_mean = FALSE, minnesota = "longrun"))

#> Call:

#> vhar_bayes(y = etf_train, num_chains = 2, num_iter = 20, coef_spec = set_ng(),

#> cov_spec = set_sv(), include_mean = FALSE, minnesota = "longrun")

#>

#> BVHAR with Stochastic Volatility

#> Fitted by Metropolis-within-Gibbs

#> Number of chains: 2

#> Total number of iteration: 20

#> Number of burn-in: 10

#> ====================================================

#>

#> Parameter Record:

#> # A draws_df: 10 iterations, 2 chains, and 188 variables

#> phi[1] phi[2] phi[3] phi[4] phi[5] phi[6] phi[7] phi[8]

#> 1 -0.12129 0.46645 0.00633 -0.2542 0.0983 -0.12326 0.8472 1.195

#> 2 -0.06070 -0.03576 0.26003 0.3627 -0.0493 0.10581 -0.6588 -0.233

#> 3 -0.12030 0.09924 0.06952 0.6217 0.2413 0.20229 -0.3341 0.896

#> 4 -0.05398 -0.83427 0.32929 -0.7151 0.5682 -0.77103 1.8176 0.311

#> 5 -0.08097 -0.00470 -0.01688 1.0261 -0.0247 0.20555 -0.7039 0.113

#> 6 -0.09683 0.00503 0.00561 0.9218 -0.3035 -0.02819 -0.8611 0.264

#> 7 -0.04152 0.00752 -0.03170 0.8207 0.4101 -0.07181 0.0765 0.490

#> 8 0.00444 -0.18934 0.07036 0.4606 0.3786 0.07076 0.0405 0.923

#> 9 -0.00374 0.07720 -0.05009 -0.0199 -0.1694 0.08192 -0.0237 1.378

#> 10 -0.04211 -0.07598 0.11729 -0.0914 0.0158 0.00741 -0.0348 1.455

#> # ... with 10 more draws, and 180 more variables

#> # ... hidden reserved variables {'.chain', '.iteration', '.draw'}Dirichlet-Laplace prior

(fit_dl <- vhar_bayes(etf_train, num_chains = 2, num_iter = 20, coef_spec = set_dl(), cov_spec = set_sv(), include_mean = FALSE, minnesota = "longrun"))

#> Call:

#> vhar_bayes(y = etf_train, num_chains = 2, num_iter = 20, coef_spec = set_dl(),

#> cov_spec = set_sv(), include_mean = FALSE, minnesota = "longrun")

#>

#> BVHAR with Stochastic Volatility

#> Fitted by Gibbs sampling

#> Number of chains: 2

#> Total number of iteration: 20

#> Number of burn-in: 10

#> ====================================================

#>

#> Parameter Record:

#> # A draws_df: 10 iterations, 2 chains, and 182 variables

#> phi[1] phi[2] phi[3] phi[4] phi[5] phi[6] phi[7]

#> 1 0.16969 -0.24454 -0.126475 -0.06212 -0.00613 0.10133 0.2047

#> 2 0.13486 -0.04642 -0.148850 0.29445 -0.00510 0.03525 0.1231

#> 3 0.09879 -0.00417 0.012937 0.08343 -0.00992 -0.03586 0.0190

#> 4 -0.05609 -0.02515 -0.009510 0.27036 -0.04458 -0.00890 -0.0160

#> 5 0.00416 0.02970 0.007852 -0.08386 -0.01198 -0.13536 0.0647

#> 6 -0.00753 -0.13360 -0.053984 0.06215 0.01830 0.02951 -0.1006

#> 7 0.03670 0.06412 -0.129178 -0.00837 0.00700 0.06118 0.1877

#> 8 0.04795 0.01647 -0.091950 0.01753 0.02061 0.03345 0.4122

#> 9 0.00318 0.01126 0.000964 0.01404 -0.00825 -0.01743 0.3645

#> 10 0.04623 -0.09924 0.000799 -0.00658 0.02443 0.00132 0.3980

#> phi[8]

#> 1 8.58e-05

#> 2 -8.17e-04

#> 3 -7.97e-04

#> 4 2.09e-03

#> 5 5.46e-03

#> 6 1.57e-02

#> 7 3.77e-01

#> 8 5.26e-01

#> 9 4.34e-01

#> 10 3.80e-01

#> # ... with 10 more draws, and 174 more variables

#> # ... hidden reserved variables {'.chain', '.iteration', '.draw'}Bayesian visualization

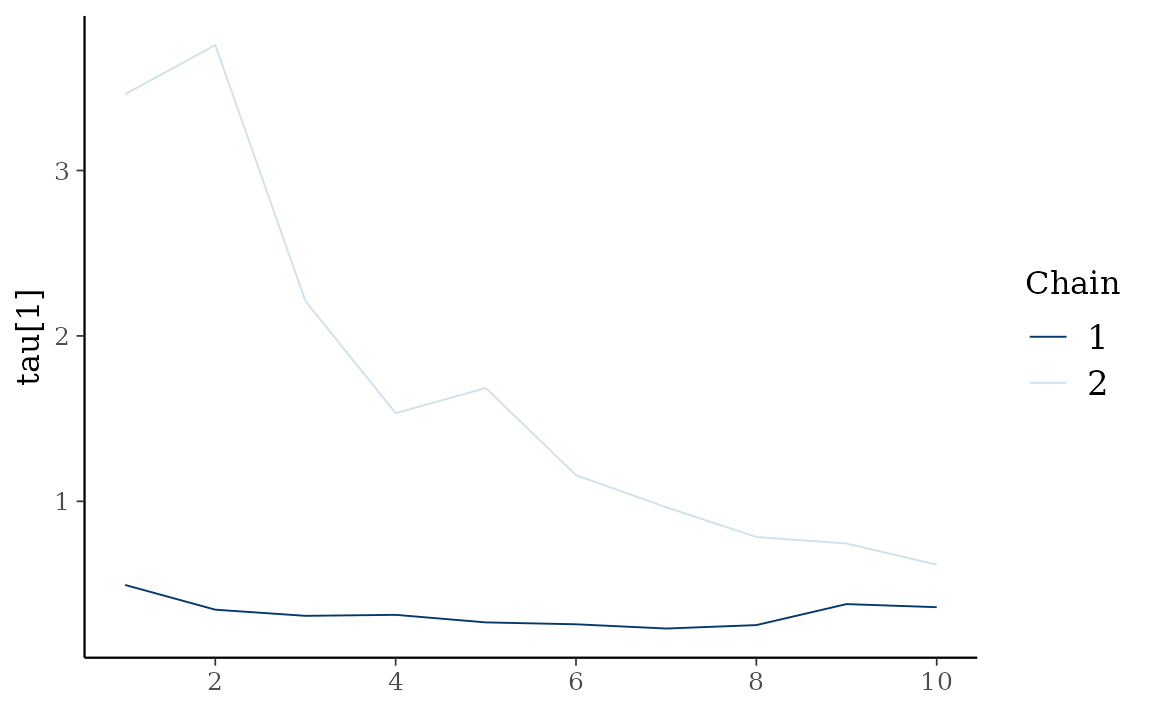

autoplot() also provides Bayesian visualization.

type = "trace" gives MCMC trace plot.

autoplot(fit_hs, type = "trace", regex_pars = "tau")

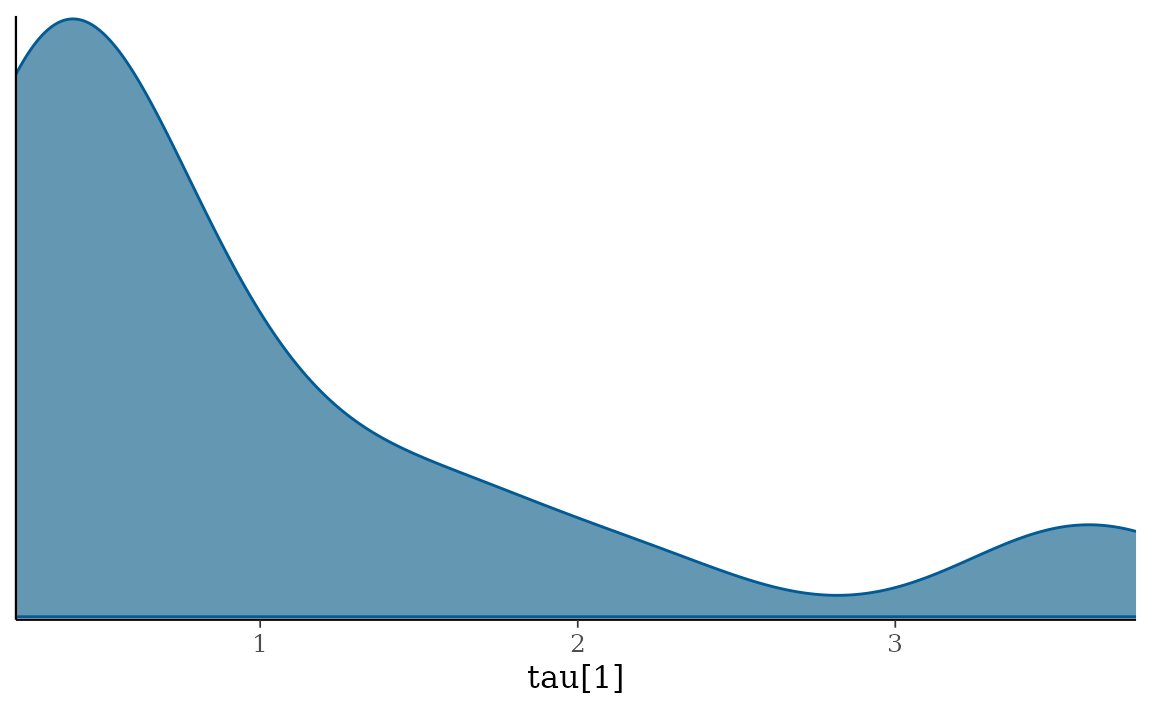

type = "dens" draws MCMC density plot.

autoplot(fit_hs, type = "dens", regex_pars = "tau")